Global Passenger xEV Battery Market In H1 2022: 195.5 GWh (Up 79%)

Just 7 xEV battery manufacturers were responsible for more than of 82% of all batteries deployed during the period.

The global passenger xEV (BEVs, PHEVs, HEVs) battery market continues its unprecedented growth in 2022, leaving 2021 results far behind.

According to Adamas Intelligence, during the first half of the year, about 195.5 GWh of battery capacity was deployed onto roads globally in all newly sold passenger xEVs. That's about 79% more than a year ago.

Batteries for commercial xEVs, energy storage systems or other applications are not included in the numbers.

That's a very high number, compared to 286 GWh deployed in the whole of 2021, and 134.5 GWh in 2020. This year will most likely end at well over 400 GWh.

If we get into the details of the "State of Charge: EVs, Batteries and Battery Materials" report, it turns out that battery-electric cars (BEVs) are responsible for 89% of all xEV batteries deployed, while non-rechargeable hybrids for just 1% (due their low battery capacity):

- BEVs: about 174.0 GWh (89% share, up from 87% a year ago)

- PHEVs: about 19.6 GWh (10% share, down from 11% a year ago)

- HEV: about 2.0 GWh (1% share, down from 2% a year ago)

- xEV: 195.5 GWh (up 79% year-over-year from 109.0 GWh a year ago)

Geographically (share):

Asia Pacific: 58% (113 GWh), up from 48% a year ago

Europe: 25% (48.1 GWh), down from 33% a year ago

Americas: 17% (33.4 GWh), down from 18% a year ago

other: 1.1%

In terms of top xEV battery cell manufacturers, we can note the dominant position of CATL and BYD approaching LG Energy Solution in the battle for the second place:

- CATL: 64.9 GWh (33% market share, up from 27% a year ago)

- LG Energy Solution: 33.8 GWh (vs 27.9 GWh a year ago)

- BYD: 24.4 GWh (up more than three-times from 7.1 GWh a year ago)

- Panasonic

- SK Innovation's SK On

- Samsung SDI

- CALB

- Gotion

- Farasis Energy

- Envision AESC: below 2.0 GWh

The top seven manufacturers control more than 82% of the market.

Lithium Iron Phosphate (LFP) has become the most popular single lithium-ion battery chemistry for passenger xEVs, although the NCM family (nickel-rich cathode), as a whole, is still in the majority:

- LFP: 52.7 GWh (27% share, up 237% year-over-year)

- NCM 5-series: 41.6 GWh (21% share)

- NCM 8-series: 36.2 GWh (19% share)

- NCM 6-series: about 23.5 GWh (12% share)

- NCA Gen 3: about 19.6 GWh (10% share)

- NCM 7-series

- NCM 111

- NCM/LMO

- NiOH

- LMO: below 1.0 GWh

If we take a look at who consumes the most batteries, it turns out that it's undoubtedly Tesla, which also sells the highest number of electric cars.

According to Adamas Intelligence, Tesla deployed nearly as much battery capacity onto roads as its four closest competitors combined (BYD, GAC, Hyundai, Kia).

- Tesla: 41.7 GWh (21.3% share)

- BYD, GAC, Hyundai, Kia: 42.7 GWh (21.8% share)

The exact number for BYD has not been disclosed in the open version of the report (probably around 24 GWh, as in the case of production), but the Chinese company has increased its battery deployment by 243% year-over-year.

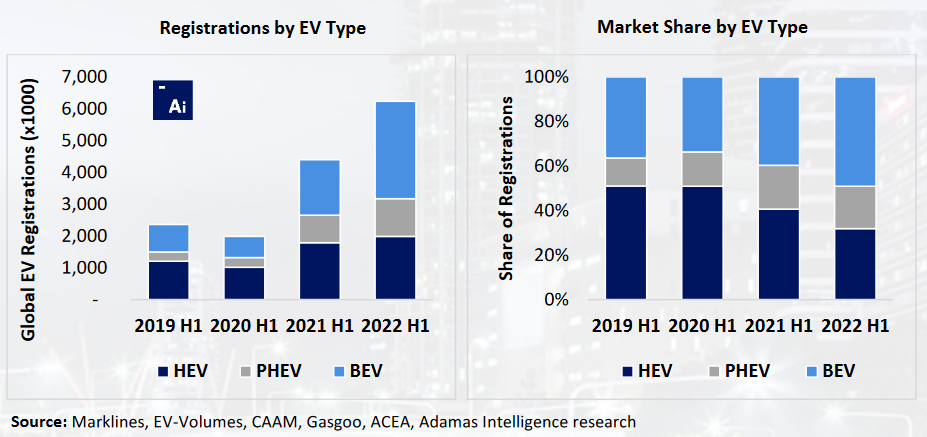

xEV registrations vs. battery deployment

The report for the first half of the year indicates that some 6.23 million new passenger xEVs were registered (up 42% year-over-year, from 4.40 million in H1 2021). We can also note that all-electric cars are gradually becoming the dominant segment:

- BEVs: about 3.05 million (49% of all xEV, up from 40% a year ago)

- PHEVs: about 1.18 million (19% of all xEV, down from 20% a year ago)

- HEV: about 1.99 million (32% of all xEV, down from 41%)

- xEV: 6.23 million (up 42% year-over-year)

*in Asia Pacific the growth amounted to 75% year-over-year

The expansion of the battery market outpaced the increase of xEV sales (again), which is not a surprise because plug-in electric cars are often equipped with bigger and bigger batteries, which adds on top of higher xEV sales.

According to Adamas Intelligence, the overall global sales-weighted average battery pack capacity of all newly sold passenger xEVs amounted to 31.4 kWh (up 27% year-over-year from 24.8 kWh.

We additionally calculated average battery pack sizes also for all of the categories, but please note that the results might be a percent or two off:

- BEVs: about 57 kWh

- PHEVs: about 16.6 kWh

- HEV: about 1 kWh

- xEV: 31.4 kWh (up 27% year-over-year from 24.8 kWh)

Interestingly, many BEVs on the market are equipped with around a 60 kWh battery.

We guess that this average number will continue to increase (for all types), because customers like to get more range, while new technologies increase energy density as well as lower costs. On the other hand, the rate of growth is expected to decrease because, at some point, enough range is enough, and better fast charging infrastructure also helps.

Battery materials

In terms of battery materials, we will focus only on general numbers, but the Adamas Intelligence's "State of Charge: EVs, Batteries and Battery Materials" report provides really interesting details.

It's worth noting that the increase of nickel, cobalt and manganese use was significantly limited by the expansion of the LFP chemistry (at the expense of NCM).

- lithium carbonate equivalent (“LCE”) - 117,200 tonnes (up 76% year-over-year)

59% as carbonate, 41% as hydroxide

*average: about 0.6 kg/kWh, about 18.8 kg/xEV (up 24%) or 34 kg/BEV - nickel - 88,200 tonnes (up 50% year-over-year)

*average: about 0.5 kg/kWh, about 14.1 kg/xEV (up 6%) - cobalt - 18,500 tonnes (up 44% year-over-year)

*average: about 0.1 kg/kWh, about 3.0 kg/xEV (up 2%) - manganese - 23,700 tonnes (up 44% year-over-year)

*average: about 0.1 kg/kWh, about 3.8 kg/xEV (up 2%) - graphite - 177,200 tonnes (up 86% year-over-year)

*average: about 0.9 kg/kWh, about 28.4 kg/xEV (up 32%)

* average numbers are only briefly estimated (not all xEVs use particular elements)

See also

RECOMMENDED FOR YOU

Toyota’s Next Generation Hybrid Batteries Promise Lower Cost, Better Performance

Tesla Burned Through Its California EV Rebate Funds In Just Five Days

Factorial Taps Hyundai Supplier To Solve Solid-State Batteries’ Biggest Problem

The Ford Fathom Will Get a $25,000 Hybrid Crossover Sibling: Report

Inside BMW's Plan To Produce The iX5’s Gigantic Battery Pack In The U.S.

Ford’s New AI Assistant Can Read Your Car’s Manual And Diagnostics

Battery Startup Raises $300 Million Promising 20% More EV Range